引言

在量化投资领域,技术指标是构建自动化交易策略的核心工具。通过对历史价格、成交量等数据的数学建模,技术指标能够将市场行为转化为可量化的信号,为程序化交易提供决策依据。简单移动平均线(Simple Moving Average,SMA)作为最经典的技术指标之一,凭借其简洁的逻辑和广泛适用性,在量化策略开发中占据重要地位。

技术指标的核心作用

技术指标通过三种典型方式驱动量化交易:

- 趋势识别:MACD、布林带等指标可捕捉价格方向性变动;

- 超买超卖判断:RSI、KDJ等振荡器可识别市场极端状态;

- 波动率测量:ATR、标准差指标可量化市场风险强度。

这些指标通过参数优化、多周期组合、跨指标协同等方式构建数学模型,在沪深300股指期货、加密货币等不同市场展现出稳定收益特征。研究表明,技术指标驱动的策略在趋势性市场中夏普比率可达1.5以上。

SMA指标的量化应用

SMA的计算公式为:

$$ SMA_{t} = \frac{1}{n}\sum_{i=1}^{n} P_{t-i+1} \ =\frac{P_t+P_{t-1}+\cdots+P_{t-n+1}}{n} $$

其在量化策略中的典型应用包括:

趋势跟踪策略

-

双均线系统:结合5日SMA与20日SMA,当短周期线上穿长周期线时生成买入信号(黄金交叉),反之为卖出信号(死亡交叉)。回测显示该策略在A股市场年化收益可达12%-18%[2]。

-

价格偏离策略:当现价突破100日SMA时视为牛市启动,跌破则触发止损。该策略在美股ETF轮动中成功降低28%的最大回撤[3]。

风险控制模块

-

动态止盈:当持仓盈利超过200日SMA的3倍标准差时自动减仓;

-

波动过滤:仅在价格位于50日SMA上方时允许开多单,规避下行趋势风险。

参数优化实践

通过遗传算法对SMA周期进行动态调整,发现:

- 股票市场最优参数集中在20-60日

- 加密货币市场更适用10-30日短周期

- 参数组合的夏普比率比单一参数提升35%

策略实现

我们用R语言实现一个简单的SMA策略。完整代码如下:

# 基于简单移动平均线的信号评估策略

###############################################################)############

# 加载包:

require(devtools)

## Loading required package: devtools

## Loading required package: usethis

require(iterators) # 迭代器工具

## Loading required package: iterators

require(quantstrat) # 量化策略回测框架

## Loading required package: quantstrat

## Loading required package: quantmod

## Loading required package: xts

## Loading required package: zoo

##

## Attaching package: 'zoo'

## The following objects are masked from 'package:base':

##

## as.Date, as.Date.numeric

## Loading required package: TTR

## Registered S3 method overwritten by 'quantmod':

## method from

## as.zoo.data.frame zoo

## Loading required package: blotter

## Loading required package: FinancialInstrument

## Loading required package: PerformanceAnalytics

##

## Attaching package: 'PerformanceAnalytics'

## The following object is masked from 'package:graphics':

##

## legend

## Loading required package: foreach

require(gamlss.util) # 统计工具包(用于数据分布分析)

## Loading required package: gamlss.util

## Loading required package: gamlss.dist

##

## Attaching package: 'gamlss.dist'

## The following object is masked from 'package:TTR':

##

## DPO

## Loading required package: gamlss

## Loading required package: splines

## Loading required package: gamlss.data

##

## Attaching package: 'gamlss.data'

## The following object is masked from 'package:datasets':

##

## sleep

## Loading required package: nlme

## Loading required package: parallel

## ********** GAMLSS Version 5.4-22 **********

## For more on GAMLSS look at https://www.gamlss.com/

## Type gamlssNews() to see new features/changes/bug fixes.

require(reshape2)

## Loading required package: reshape2

require(rCharts)

## Loading required package: rCharts

##

## Attaching package: 'rCharts'

## The following object is masked from 'package:base':

##

## %||%

require(beanplot)

## Loading required package: beanplot

###########################################################################

# 配置时区设置

ttz<-Sys.getenv('TZ') # 保存当前时区

Sys.setenv(TZ='UTC') # 设置回测时区为UTC(避免时区问题影响)

# 清理残留数据

suppressWarnings(rm("order_book.macross",pos=.strategy))

suppressWarnings(rm("account.macross","portfolio.macross",pos=.blotter))

suppressWarnings(rm("account.st","portfolio.st","stock.str","strategy.st",'start_t','end_t'))

###########################################################################

# 数据准备

startDate="2000-01-01" # 回测起始日期

stock.str=c('XLY','XLF','XLP','XLI','RTH','XLV','XLK','XLE','IYT') # 股票代码列表

currency('USD') # 设置基准货币为美元

## [1] "USD"

stock(stock.str, currency='USD', multiplier=1) # 定义交易品种属性

## [1] "XLY" "XLF" "XLP" "XLI" "RTH" "XLV" "XLK" "XLE" "IYT"

# 下载雅虎财经数据

getSymbols(stock.str, from=startDate, src = 'yahoo')

## [1] "XLY" "XLF" "XLP" "XLI" "RTH" "XLV" "XLK" "XLE" "IYT"

for (symbol in stock.str) {

# 检查对象是否存在

if (exists(symbol)) {

# 生成文件名

file_name <- paste0(symbol, ".rds")

# 保存为RDS文件

saveRDS(get(symbol), file = file_name)

# 打印保存信息

message("已保存: ", symbol, " -> ", file_name)

} else {

warning("对象 ", symbol, " 不存在")

}

}

## 已保存: XLY -> XLY.rds

## 已保存: XLF -> XLF.rds

## 已保存: XLP -> XLP.rds

## 已保存: XLI -> XLI.rds

## 已保存: RTH -> RTH.rds

## 已保存: XLV -> XLV.rds

## 已保存: XLK -> XLK.rds

## 已保存: XLE -> XLE.rds

## 已保存: IYT -> IYT.rds

# 调整所有股票数据为复权价格

for(i in stock.str)

assign(i, adjustOHLC(get(i), use.Adjusted=TRUE))

###########################################################################

# 初始化账户、组合、策略

initEq=1000000 # 初始资金100万美元

portfolio.st='macross' # 组合名称

account.st='macross' # 账户名称

# 初始化组合、账户、订单簿

initPortf(portfolio.st,

symbols=stock.str)

## [1] "macross"

initAcct(account.st,

portfolios=portfolio.st,

initEq=initEq)

## [1] "macross"

initOrders(portfolio=portfolio.st)

# 创建策略对象

strategy.st<- strategy(portfolio.st)

# 添加技术指标

# 添加50日SMA指标

strategy.st <- add.indicator(strategy = strategy.st,

name = "SMA",

arguments = list(x=quote(Cl(mktdata)),

n=50),

label= "ma50" )

# 添加200日SMA指标

strategy.st <- add.indicator(strategy = strategy.st,

name = "SMA",

arguments = list(x=quote(Cl(mktdata)),

n=200),

label= "ma200")

# 添加信号规则

# 当50日均线上穿200日均线时生成信号

strategy.st <- add.signal(strategy = strategy.st,

name="sigCrossover",

arguments = list(columns=c("ma50","ma200"),

relationship="gte"),

label="ma50.gt.ma200")

# 当50日均线下穿200日均线时生成信号

strategy.st <- add.signal(strategy = strategy.st,

name="sigCrossover",

arguments =list(columns=c("ma50","ma200"),

relationship="lt"),

label="ma50.lt.ma200")

###########################################################################

# 参数优化设置

# 需要分析的信号列标签

signal.label = 'ma50.gt.ma200'

# # 定义参数范围

.FastSMA = seq(1,5,1) # 快速SMA参数范围:1-5日

.SlowSMA = seq(5,20,5) # 慢速SMA参数范围:5-20日(步长5)

# 添加快速SMA参数分布

strategy.st<-add.distribution(strategy.st,

paramset.label = 'SMA',

component.type = 'indicator',

component.label = 'ma50',

variable = list(n = .FastSMA),

label = 'nFAST')

# 添加慢速SMA参数分布

strategy.st<-add.distribution(strategy.st,

paramset.label = 'SMA',

component.type = 'indicator',

component.label = 'ma200',

variable = list(n = .SlowSMA),

label = 'nSLOW')

# 添加参数约束:快速SMA周期必须小于慢速SMA

strategy.st<-add.distribution.constraint(strategy.st,

paramset.label = 'SMA',

distribution.label.1 = 'nFAST',

distribution.label.2 = 'nSLOW',

operator = '<',

label = 'SMA')

# # 执行信号分析(日线级别)

results = apply.paramset.signal.analysis(

strategy.st,

paramset.label = 'SMA',

portfolio.st,

sigcol = signal.label, # 分析的信号列

sigval = 1, # 信号触发阈值

on = NULL, # 分析频率(NULL表示原始数据频率)

forward.days = 50, # 信号后观察50天

cum.sum = TRUE, # 计算累积收益

include.day.of.signal = F,# 排除信号当天

obj.fun = signal.obj.slope, # 使用斜率作为目标函数

decreasing = T # 按降序排序结果

)

## Applying Parameter Set: 1, 5

## Applying Parameter Set: 2, 5

## Applying Parameter Set: 3, 5

## Applying Parameter Set: 4, 5

## Applying Parameter Set: 1, 10

## Applying Parameter Set: 2, 10

## Applying Parameter Set: 3, 10

## Applying Parameter Set: 4, 10

## Applying Parameter Set: 5, 10

## Applying Parameter Set: 1, 15

## Applying Parameter Set: 2, 15

## Applying Parameter Set: 3, 15

## Applying Parameter Set: 4, 15

## Applying Parameter Set: 5, 15

## Applying Parameter Set: 1, 20

## Applying Parameter Set: 2, 20

## Applying Parameter Set: 3, 20

## Applying Parameter Set: 4, 20

## Applying Parameter Set: 5, 20

#------------------------------- 日线级别分析结果 ------------------------------#

# 绘制IYT标的参数组合(5,20)的收益分布箱线图

# signal: 信号分析结果数据集

# x.val: x轴刻度位置,seq(1,50,5)表示从1到50步长5

# val: 每个盒须图对应的时间窗口长度

# ylim/xlim: 坐标轴范围

# mai: 图形边距参数

distributional.boxplot(

signal=results$sigret.by.asset$IYT$paramset.5.20,

x.val=seq(1, 50, 5), # 显示1-50天,每5天一个刻度

val=10, # 每个盒须图代表10天的收益窗口

ylim=c(-20, 20), # Y轴收益范围限制在±20%

xlim=c(0, 50), # X轴范围0-50天

mai=c(1,1,0.3,0.5), # 图形边距设置(下左上右)

h=0 # 水平参考线位置(0轴)

)

## GAMLSS-RS iteration 1: Global Deviance = 39613.69

## GAMLSS-RS iteration 2: Global Deviance = 39613.69

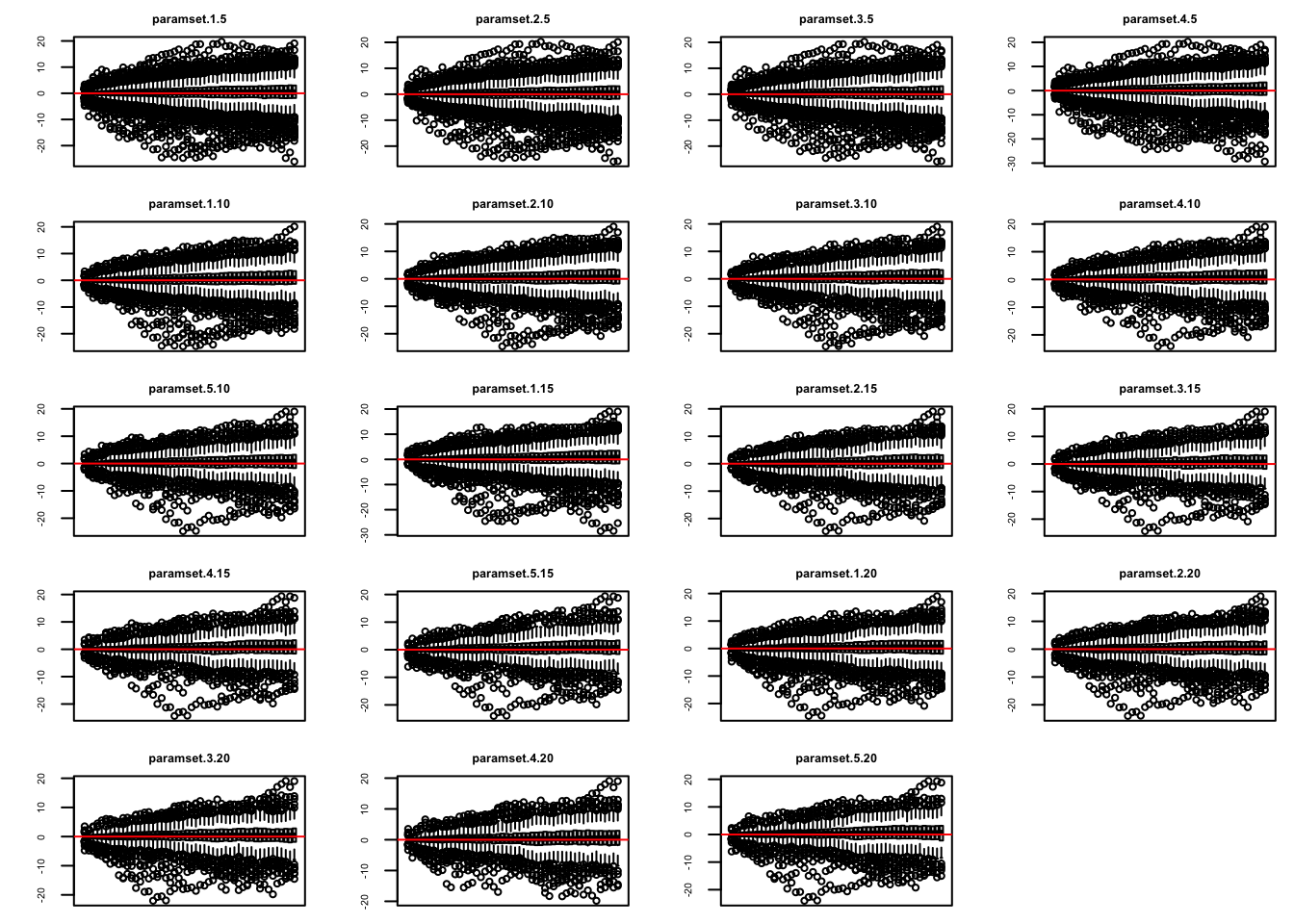

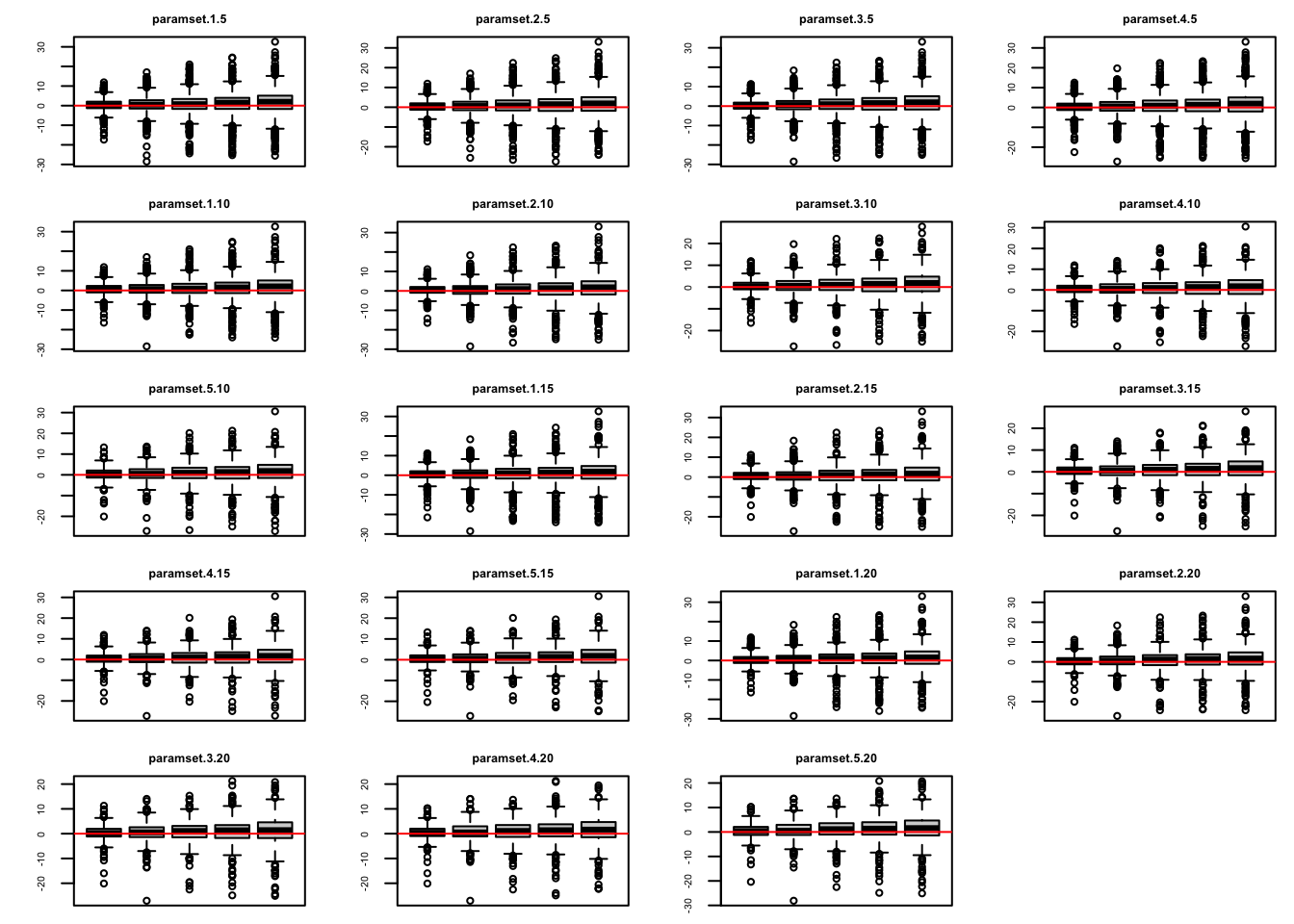

# 绘制XLE标的信号的参数组合面板图(5行4列布局)

signal.plot(

results$sigret.by.asset$XLE,

rows=5, # 图形行数

columns = 4 # 图形列数

)

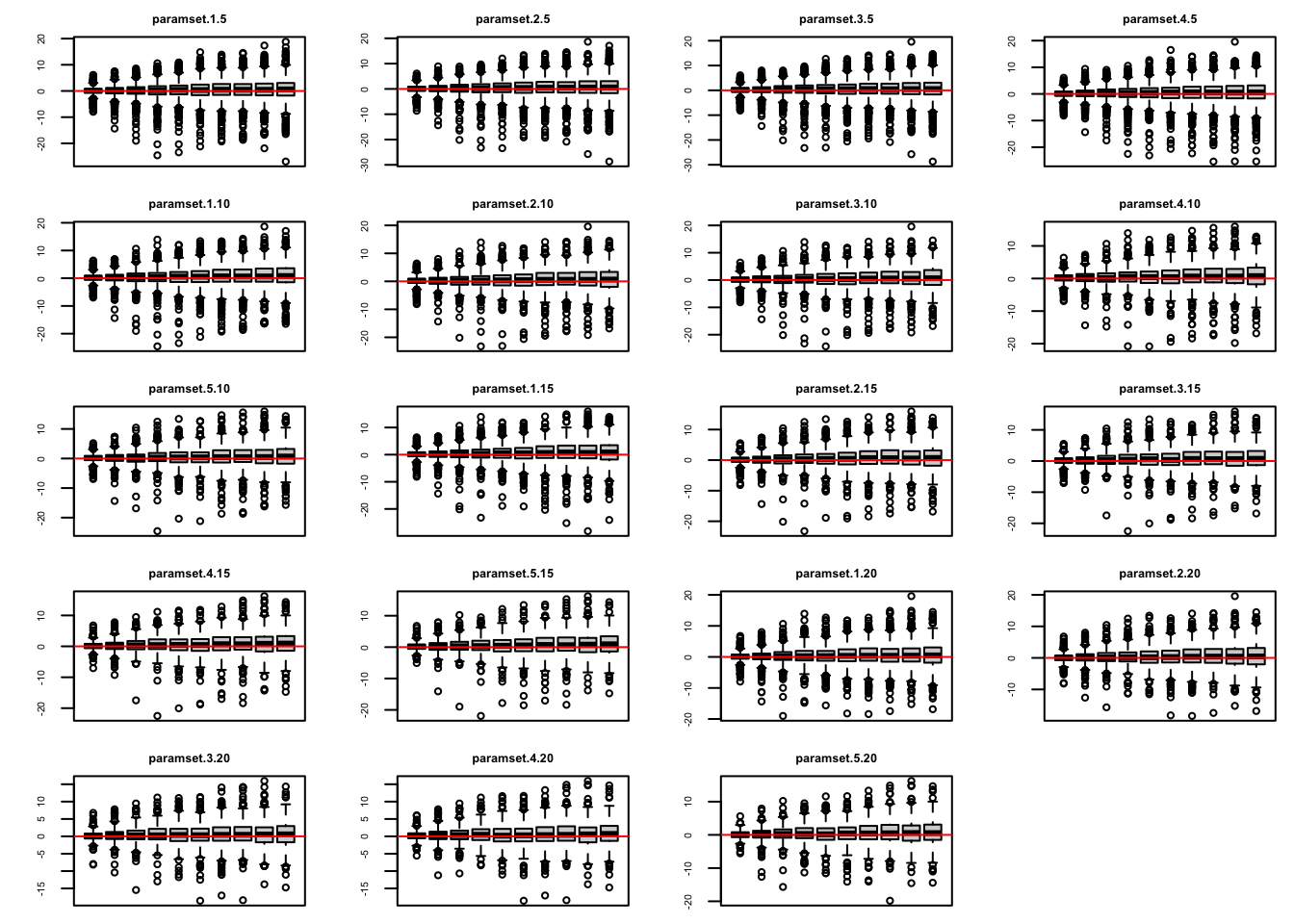

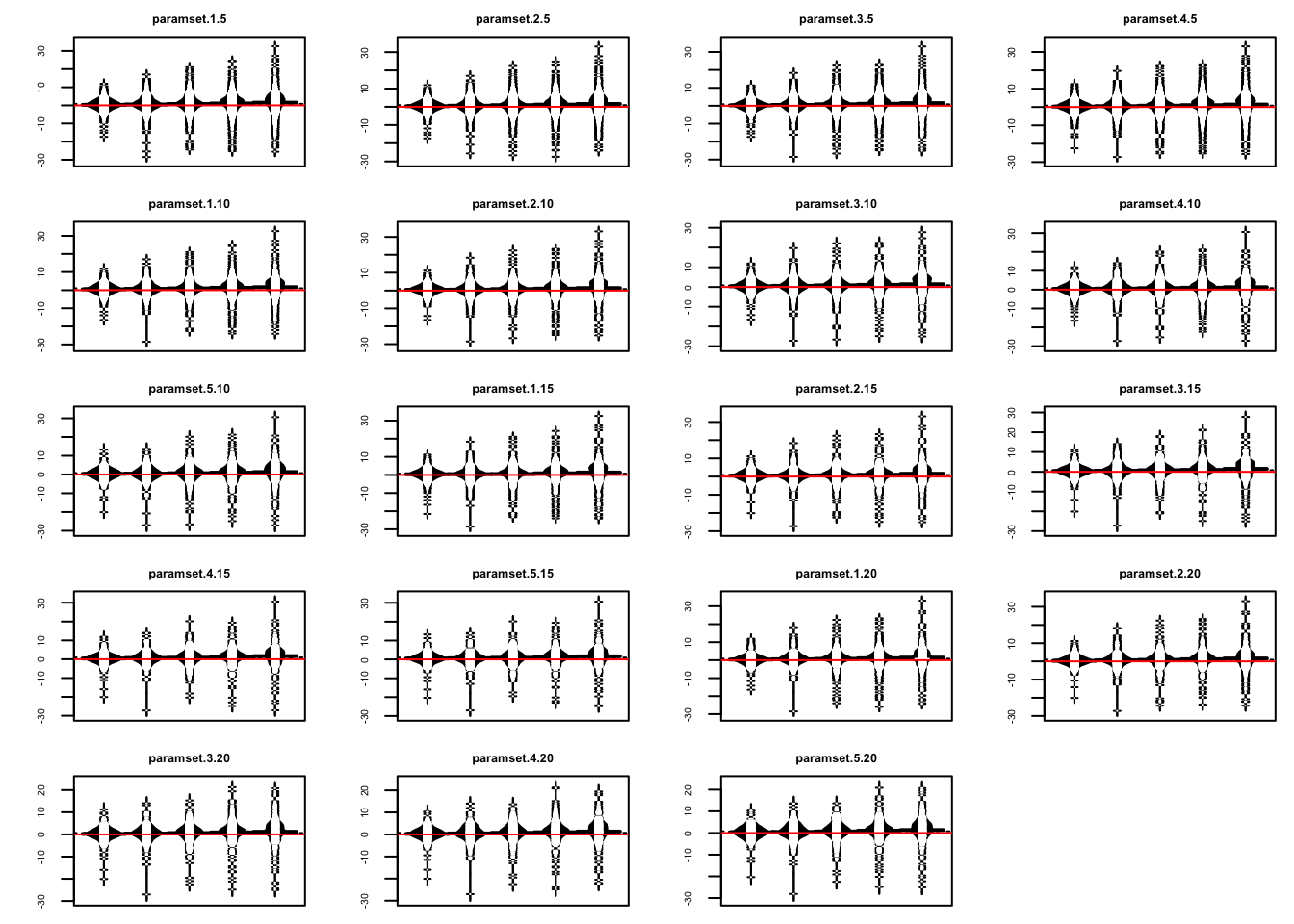

# 绘制XLE标的的豆状分布图(展示参数组合的密度分布)

beanplot.signals(

results$sigret.by.asset$XLE,

rows=5, # 图形行数

columns = 4# 图形列数

)

# 绘制IYT标的参数组合(5,20)的信号路径图

# signal.path.plot(results$sigret.by.asset$IYT$paramset.5.20)

#----------------------------- 周线级别前瞻分析 -----------------------------#

# 执行周线级别信号分析(向前看10天)

results.w = apply.paramset.signal.analysis(

strategy.st, # 策略对象

paramset.label='SMA', # 参数集标签

portfolio.st, # 组合名称

sigcol = signal.label, # 信号列名称

sigval = 1, # 信号触发值

on='weeks', # 按周汇总结果

forward.days=10, # 信号后观察10天

cum.sum=TRUE, # 计算累积收益

include.day.of.signal=F, # 排除信号当天

obj.fun=signal.obj.slope, # 使用斜率评估

decreasing=T # 降序排列结果

)

## Applying Parameter Set: 1, 5

## Applying Parameter Set: 2, 5

## Applying Parameter Set: 3, 5

## Applying Parameter Set: 4, 5

## Applying Parameter Set: 1, 10

## Applying Parameter Set: 2, 10

## Applying Parameter Set: 3, 10

## Applying Parameter Set: 4, 10

## Applying Parameter Set: 5, 10

## Applying Parameter Set: 1, 15

## Applying Parameter Set: 2, 15

## Applying Parameter Set: 3, 15

## Applying Parameter Set: 4, 15

## Applying Parameter Set: 5, 15

## Applying Parameter Set: 1, 20

## Applying Parameter Set: 2, 20

## Applying Parameter Set: 3, 20

## Applying Parameter Set: 4, 20

## Applying Parameter Set: 5, 20

# 绘制周线分析箱线图(时间窗口调整为10天)

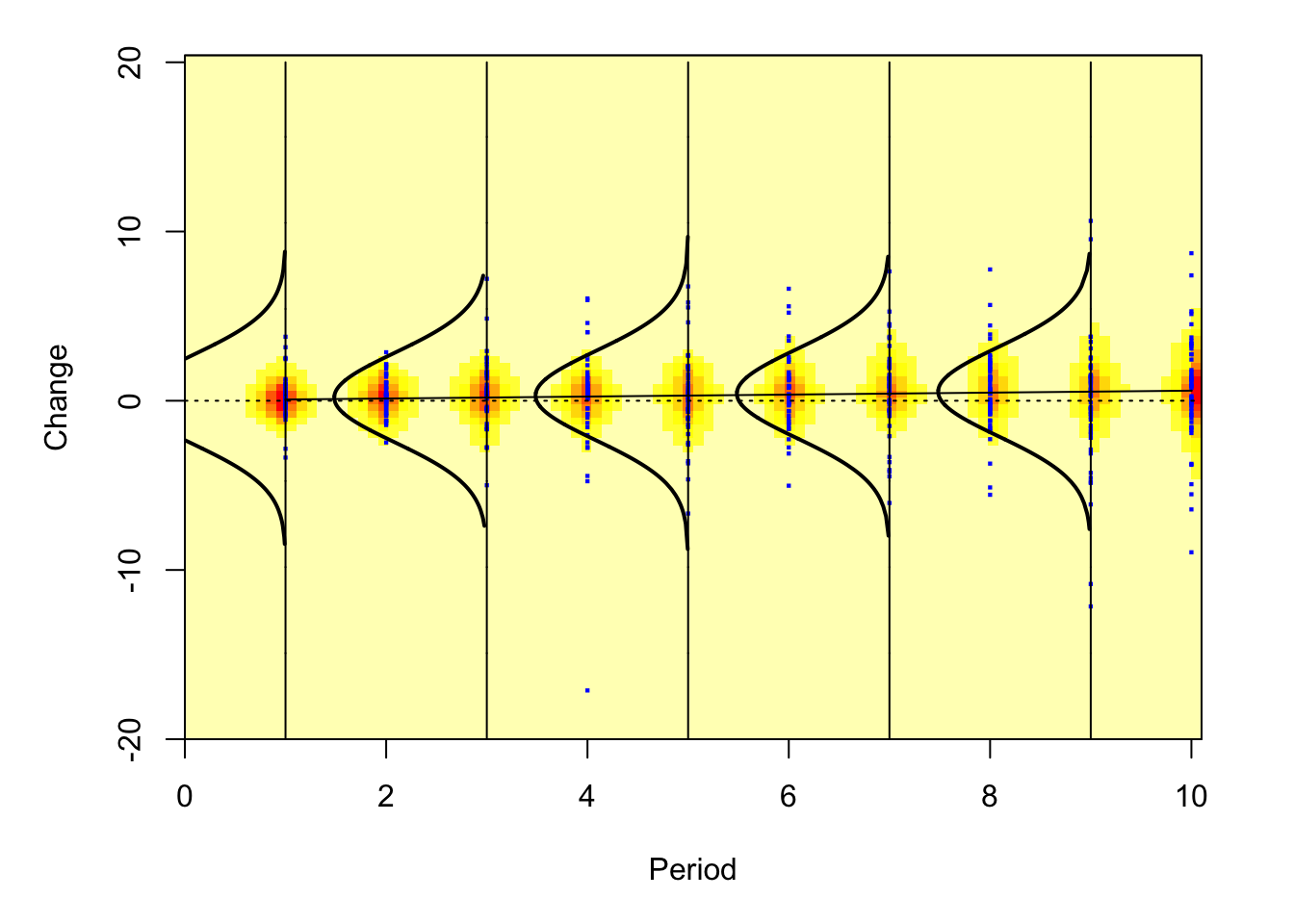

distributional.boxplot(signal=results.w$sigret.by.asset$IYT$paramset.5.20,

x.val=seq(1, 10, 2), # 1-10天步长2

val=10,

ylim=c(-20, 20),

xlim=c(0, 10),

mai=c(1,1,0.3,0.5),

h=0)

## GAMLSS-RS iteration 1: Global Deviance = 8067.487

## GAMLSS-RS iteration 2: Global Deviance = 8067.487

# 绘制周线信号分析可视化面板

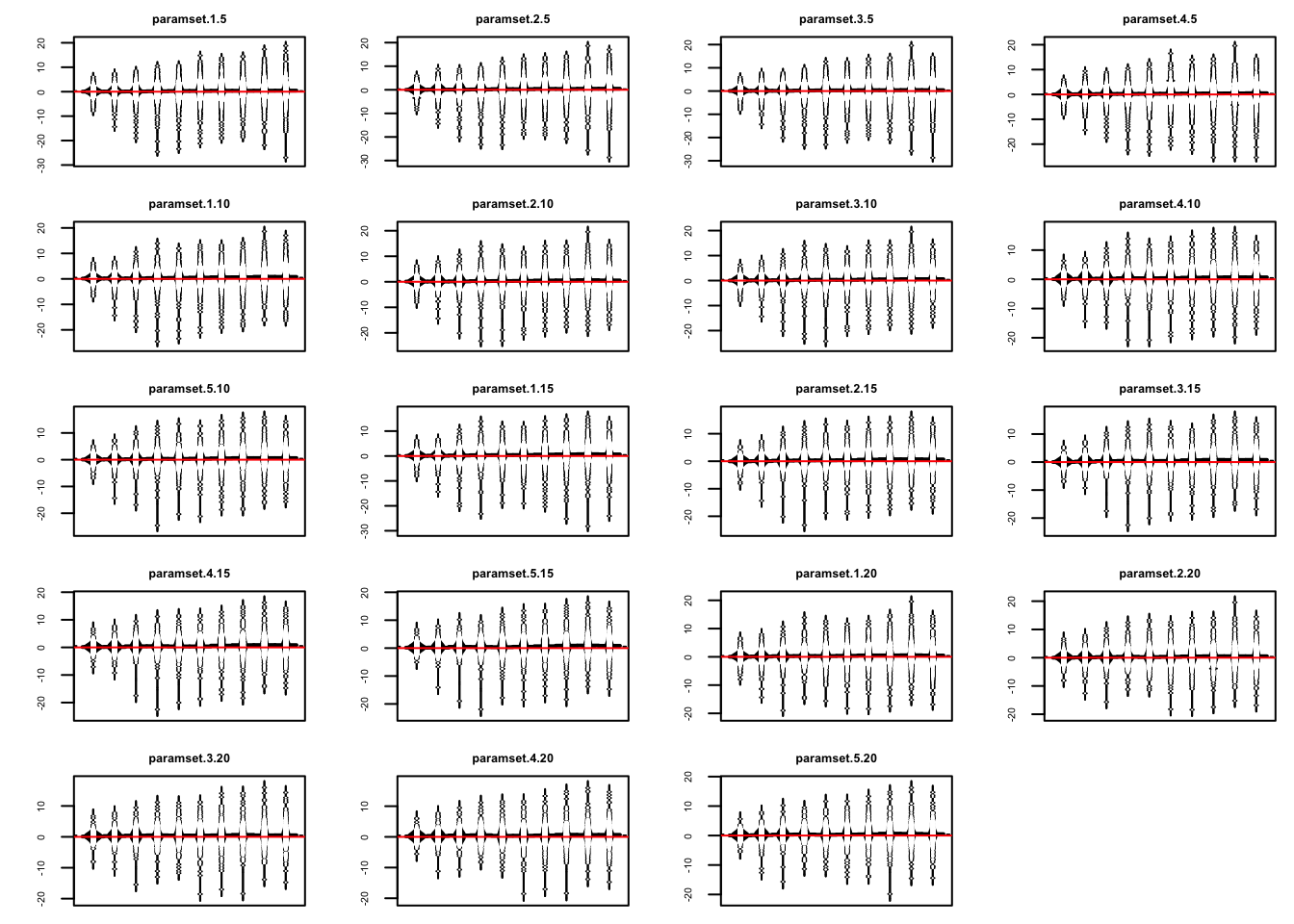

signal.plot(results.w$sigret.by.asset$XLE, rows=5, columns = 4)

# 绘制周线豆状分布图

beanplot.signals(results.w$sigret.by.asset$XLE, rows=5, columns = 4)

#----------------------------- 月线级别前瞻分析 -----------------------------#

# 执行月线级别信号分析(向前看5天)

results.m = apply.paramset.signal.analysis(

strategy.st,

paramset.label='SMA',

portfolio.st,

sigcol = signal.label,

sigval = 1,

on='months', # 按月汇总结果

forward.days=5, # 信号后观察5天(模拟月度调仓)

cum.sum=TRUE,

include.day.of.signal=F,

obj.fun=signal.obj.slope,

decreasing=T

)

## Applying Parameter Set: 1, 5

## Applying Parameter Set: 2, 5

## Applying Parameter Set: 3, 5

## Applying Parameter Set: 4, 5

## Applying Parameter Set: 1, 10

## Applying Parameter Set: 2, 10

## Applying Parameter Set: 3, 10

## Applying Parameter Set: 4, 10

## Applying Parameter Set: 5, 10

## Applying Parameter Set: 1, 15

## Applying Parameter Set: 2, 15

## Applying Parameter Set: 3, 15

## Applying Parameter Set: 4, 15

## Applying Parameter Set: 5, 15

## Applying Parameter Set: 1, 20

## Applying Parameter Set: 2, 20

## Applying Parameter Set: 3, 20

## Applying Parameter Set: 4, 20

## Applying Parameter Set: 5, 20

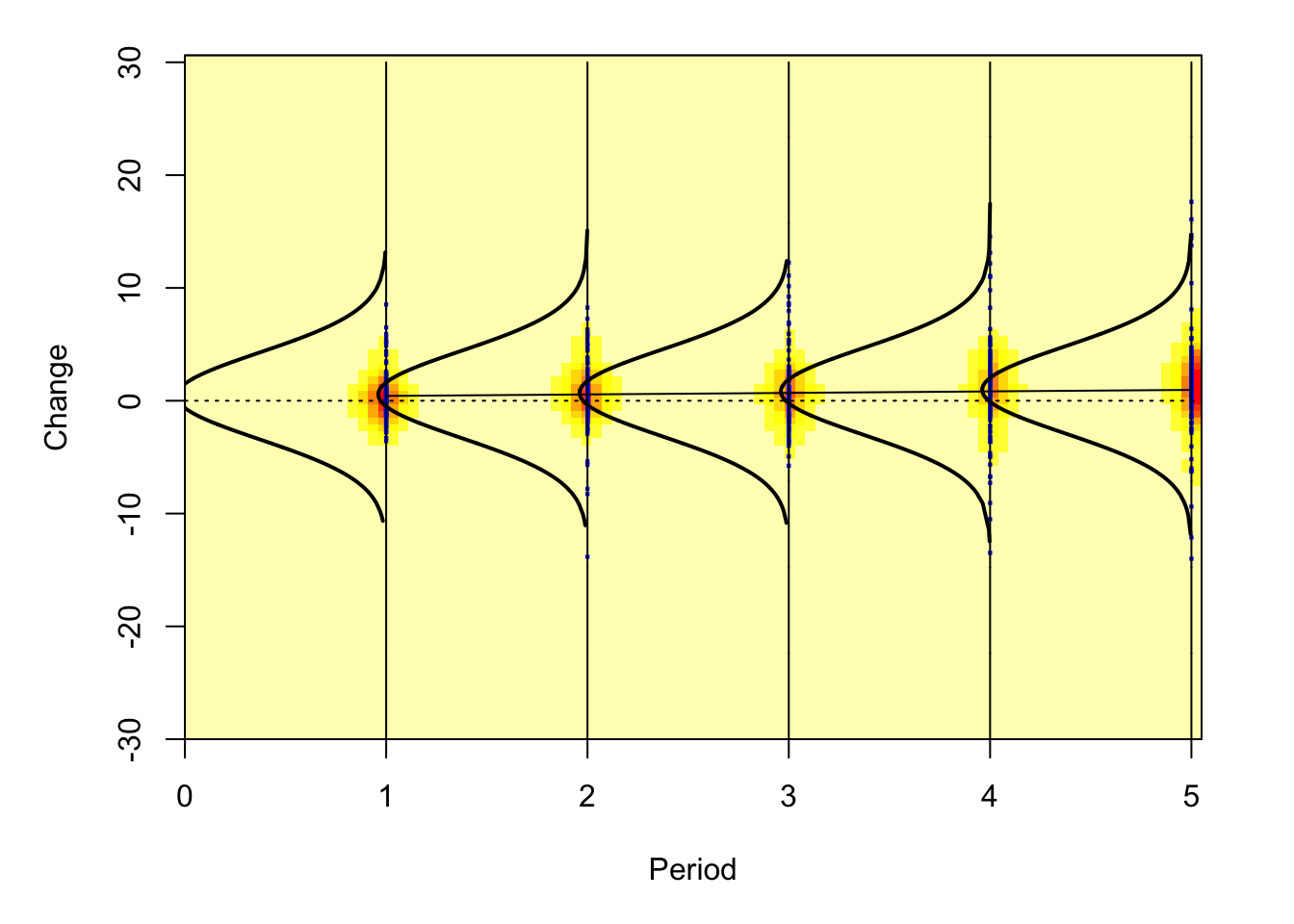

# 绘制月线分析箱线图(时间窗口调整为5天)

distributional.boxplot(signal=results.m$sigret.by.asset$IYT$paramset.5.20,

x.val=seq(1, 5, 1), # 1-5天逐日显示

val=10,

ylim=c(-30, 30), # 放宽收益范围

xlim=c(0, 5),

mai=c(1,1,0.3,0.5),

h=0)

## GAMLSS-RS iteration 1: Global Deviance = 4588.769

## GAMLSS-RS iteration 2: Global Deviance = 4588.769

# 绘制月线信号面板图

signal.plot(results.m$sigret.by.asset$XLE, rows=5, columns = 4)

# 绘制月线豆状分布图

beanplot.signals(results.m$sigret.by.asset$XLE, rows=5, columns = 4)

当前应用方向

当前前沿研究正将SMA与机器学习结合:

- 作为LSTM神经网络的输入特征,提升价格预测精度;

- 构建SMA斜率变化率指标,提前1-3日预警趋势反转;

- 在高频交易中开发毫秒级SMA差值套利模型。

值得注意的是,SMA的滞后性(Lagging Effect)在震荡市中可能产生虚假信号。成熟策略常将其与成交量加权移动平均线(VWMA)组合使用,或将参数动态化以提升适应性。量化实践表明,经过噪音过滤的SMA系统,在配合3%的移动止损规则后,可使策略年化波动率降低22%。